2025 is shaping up to be a turning point for real estate in New Zealand, offering new challenges and opportunities for buyers, investors, and professionals alike. This essential guide delivers the latest insights, expert advice, and practical steps tailored to the dynamic property market ahead. You will uncover emerging trends, understand regulatory shifts, and explore proven strategies for navigating buying, selling, and investing. Whether you are looking to purchase your first home or grow your property portfolio, this resource provides the clarity and confidence needed to make informed decisions in a rapidly evolving landscape.

The 2025 New Zealand Real Estate Market Landscape

The landscape for real estate in new zealand is undergoing significant transformation in 2025. Economic shifts, evolving buyer preferences, and regulatory updates are all shaping the market in unique ways. Understanding these changes is crucial for informed decision making, whether you are buying, selling, or investing.

Key Market Trends and Forecasts

The year 2025 is marked by robust GDP growth and steady employment rates, boosting confidence in real estate in new zealand. Auckland remains the country’s largest and most active market, but Wellington and Christchurch are also seeing solid growth. Emerging hotspots such as Tauranga and Hamilton are gaining traction, driven by affordability and improved infrastructure.

A notable shift is the increasing demand for regional properties. Many buyers, influenced by remote work trends, are prioritising lifestyle and space over proximity to city centres. This is creating strong competition in areas previously considered secondary markets.

Sustainability is now a core focus in real estate in new zealand. Eco-friendly and energy-efficient developments are highly sought after, reflecting both consumer demand and government incentives for green building. Queenstown stands out with a luxury property boom, attracting both domestic and international buyers seeking premium lifestyle options.

International investment remains significant, though foreign buyer rules continue to evolve. Recent adjustments to these rules have redirected some overseas interest towards high-end and new-build properties. According to the CBRE New Zealand Real Estate Market Outlook 2025, median house prices held steady in early 2025, with national averages just above $800,000. Days on market have lengthened slightly, reflecting a more balanced environment, while rental yields in key centres range from 3.5% to 5%.

| Region | Median Price (NZD) | Days on Market | Rental Yield (%) |

|---|---|---|---|

| Auckland | $1,020,000 | 38 | 3.7 |

| Wellington | $860,000 | 35 | 4.1 |

| Christchurch | $710,000 | 32 | 4.3 |

| Queenstown | $1,550,000 | 29 | 3.5 |

| Tauranga | $820,000 | 34 | 4.0 |

These trends highlight the dynamic nature of real estate in new zealand for 2025.

Regulatory and Policy Changes

Government policies continue to play a pivotal role in shaping real estate in new zealand. Recent initiatives focus on boosting housing supply, supporting first-home buyers, and enhancing rental quality. Changes to foreign ownership laws have tightened criteria for non-residents, particularly in residential sectors.

Taxation updates are front of mind for both investors and home buyers. The bright-line test has been extended, meaning capital gains tax applies if investment properties are sold within a set period. Property tax adjustments and stricter rules around interest deductibility are influencing investor behaviour.

Landlords and property managers must comply with updated standards, such as the Healthy Homes Standards, which set minimum requirements for heating, ventilation, and insulation in rentals. These regulations aim to improve tenant wellbeing and the overall quality of real estate in new zealand. For example, landlords now face specific deadlines to meet compliance, and failure to do so can result in significant penalties.

Compliance requirements are also increasing for new developments and body corporates, ensuring that safety, environmental, and transparency standards are maintained. Staying informed about these changes is essential for anyone involved in real estate in new zealand, as the regulatory environment continues to evolve rapidly.

Navigating the Buying Process in 2025

Navigating the buying process for real estate in new zealand in 2025 requires a fresh approach. The evolving market landscape, new lending criteria, and updated regulations mean buyers must be more informed and strategic than ever. Whether you are a first-time buyer or a seasoned investor, understanding each step will help you make confident decisions and avoid costly mistakes.

Step 1: Assessing Your Needs and Budget

The first step in buying real estate in new zealand is to define your property goals. Are you seeking a home for your family, or is this an investment? Your answer will influence everything from property type to location.

Next, calculate your budget. Lenders in 2025 continue to require at least a 20% deposit for most buyers, but some first-home schemes may accept less. Use online mortgage calculators to estimate repayments and understand how much you can borrow.

Consider the Loan-to-Value Ratio (LVR), which impacts how much you need upfront. For first-home buyers, a lower LVR can mean more favourable lending terms. Assess your income, existing debts, and ongoing expenses to determine what is realistically affordable in today’s market.

Budget Planning Tools:

- Online mortgage calculators

- Bank affordability checklists

- Property goal worksheets

Taking time to clarify your needs and budget ensures you start your real estate in new zealand journey on solid ground.

Step 2: Researching the Market

With your goals and budget set, research is your next priority. Use reputable online platforms and local real estate agents to scan available listings. Pay close attention to neighbourhood factors like school zones, amenities, and public transport links.

Review comprehensive property reports and Land Information Memorandums (LIMs) to uncover any issues with a property. Comparing regions is also vital. For example, Auckland may offer more urban amenities, while Tauranga is popular for family-friendly suburbs and lifestyle properties.

Stay up to date with market statistics and trends. The REINZ March 2025 Property Report provides invaluable insights into median prices, days on market, and inventory levels across New Zealand.

Key Market Comparison Table:

| City | Median Price (2025) | Avg. Days on Market | Rental Yield (%) |

|---|---|---|---|

| Auckland | $1,000,000 | 38 | 3.6 |

| Wellington | $830,000 | 29 | 4.1 |

| Tauranga | $900,000 | 35 | 3.8 |

Thorough research sets the foundation for a successful real estate in new zealand purchase.

Step 3: Securing Finance

Securing finance is a critical step in the real estate in new zealand process. In 2025, buyers can choose from a range of mortgage products, including fixed, floating, and offset loans. Each comes with its own advantages depending on your financial situation and risk tolerance.

Banks remain the primary lenders, but non-bank options are increasingly popular for those with unique circumstances or lower deposits. Start by obtaining a mortgage pre-approval, which clarifies your borrowing limit and strengthens your position when making an offer.

Interest rates in 2025 are expected to fluctuate, so monitor trends closely. Seek advice on whether to lock in a fixed rate or opt for a floating rate that may offer lower payments but greater risk.

Finance Checklist:

- Compare mortgage products

- Gather required documents (income, ID, proof of deposit)

- Obtain pre-approval before house hunting

Being finance-ready positions you to act quickly in the competitive real estate in new zealand market.

Step 4: Making an Offer and Closing the Deal

Once you find the right property, it’s time to make an offer. Sale types include auction, tender, or direct negotiation. Each method has unique rules and timelines, so consult your agent or legal adviser to understand the process.

Legal due diligence is essential. Review the property’s title, complete a building inspection, and ensure the sale and purchase agreement protects your interests. The settlement process typically takes several weeks, involving final checks, transferring funds, and official handover.

Common Pitfalls for First-Time Buyers:

- Overlooking hidden property issues

- Misunderstanding auction terms

- Failing to secure finance in time

Stay organised and proactive throughout this final step. Closing your real estate in new zealand deal smoothly is the reward for thorough preparation and informed decision-making.

Property Investment Strategies for 2025

Investing in real estate in new zealand in 2025 demands a strategic approach. The landscape is dynamic, shaped by evolving market forces, changing regulations, and shifting buyer preferences. Whether you’re a seasoned investor or considering your first property, understanding the current climate is essential for success.

Identifying Profitable Opportunities

The key to successful investment in real estate in new zealand is recognising where demand and growth intersect. Median house prices across major regions like Auckland and Wellington remain strong, but emerging hotspots such as Rotorua and Hamilton are drawing attention for their affordability and strong rental yields.

When evaluating opportunities, consider high-demand property types. Townhouses and apartments offer lower maintenance and appeal to urban professionals, while lifestyle blocks are in demand for those seeking more space. Regional centres are seeing population growth due to remote work trends, increasing the attractiveness of properties outside main cities.

Short-term rental markets are also thriving. Rotorua, for example, has seen a surge in demand for holiday accommodation, with investors capitalising on tourism and domestic travel trends. Analysing rental yields and capital growth potential is crucial—use online tools and market reports to compare regions and property types.

If you’re just starting out, the Getting started as a property investor guide offers step-by-step insights tailored to the unique conditions of real estate in new zealand.

Risk Management and Diversification

A balanced portfolio is essential in real estate in new zealand, as market conditions can shift quickly. Diversifying across regions, property types, and tenant profiles helps spread risk and ensure stable returns.

Vacancy rates, maintenance costs, and market downturns are the primary risks investors face. Regular property inspections and proactive maintenance can help avoid costly surprises. Insurance options such as landlord, building, and income protection insurance are increasingly important, especially as weather events and compliance standards evolve.

Consider the example of a Wellington investor who diversified by acquiring both residential and commercial properties. This approach offered resilience when the residential market cooled, as commercial tenancies provided steady income. Monitoring local developments and staying informed on regulatory changes can further protect your investment in real estate in new zealand.

Legal and Tax Considerations

Navigating the legal and tax environment is a cornerstone of successful investing in real estate in new zealand. Investors must keep up with obligations such as the bright-line test, capital gains tax rules, and ongoing property taxes.

Ownership structures can impact your tax liability and asset protection. Individuals, partnerships, and trusts each offer different advantages and responsibilities. Compliance requirements, including Healthy Homes Standards and tenancy reforms, are non-negotiable for rental property owners.

For example, selling an investment property within the bright-line period may trigger significant tax liabilities. It’s vital to seek professional advice and stay updated with legislative changes to avoid costly mistakes. By understanding these factors, you can make informed decisions and maximise returns from real estate in new zealand.

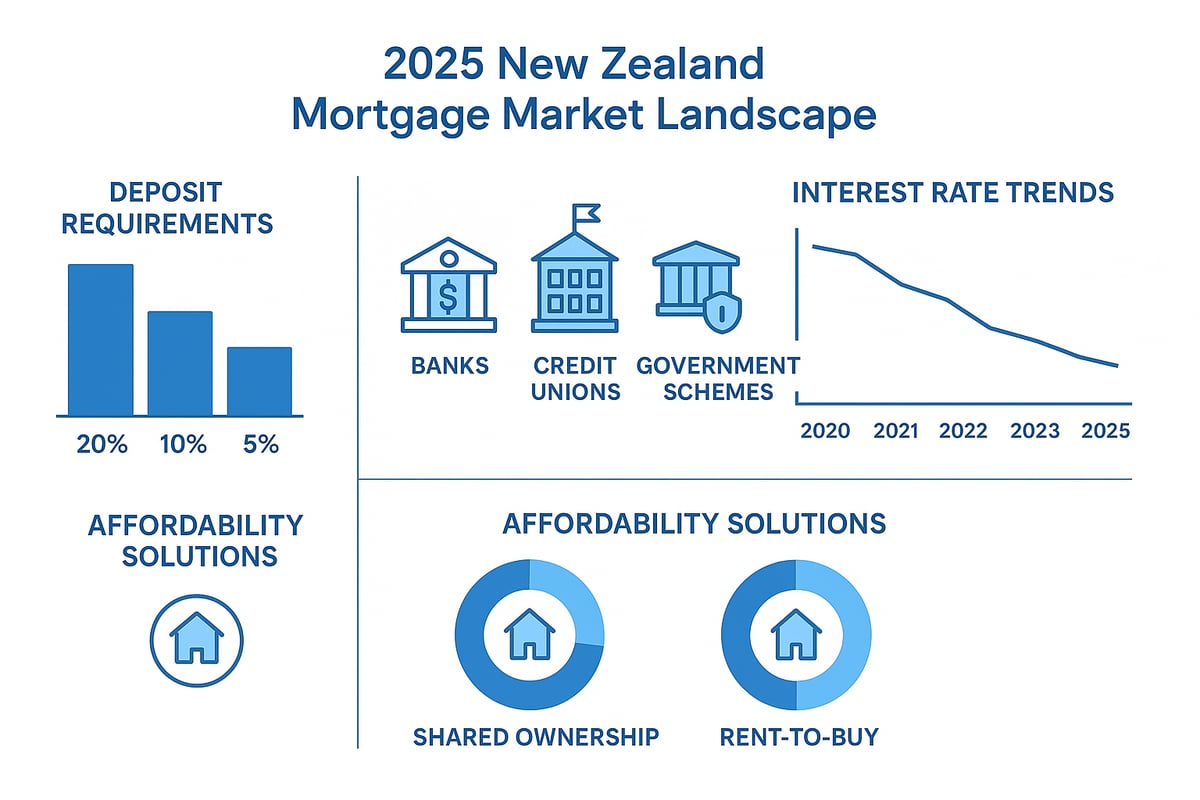

Financing, Mortgages, and Affordability in 2025

Securing the right finance is a critical step for anyone involved in real estate in new zealand. The lending landscape in 2025 is evolving rapidly, with new regulations and products shaping how buyers and investors approach property ownership. Understanding your options and challenges is essential to making informed decisions in this dynamic market.

Mortgage Market Overview

The 2025 mortgage market in New Zealand is more diverse than ever. Major banks continue to dominate, but credit unions and new financial entrants are offering innovative products. Typical deposit requirements remain at 20 percent for most buyers, while loan-to-value ratio (LVR) restrictions are being monitored closely by the Reserve Bank to ensure market stability.

Government assistance programmes, such as the First Home Grant and Kāinga Ora, are helping eligible buyers enter the market. These schemes provide valuable support, especially for first-time buyers navigating real estate in new zealand. According to DLA Piper Real Estate Trends 2025, evolving lending criteria and sustainability initiatives are influencing the types of properties being financed.

| Lender Type | Typical Deposit | Notable Features |

|---|---|---|

| Major Banks | 20% | Wide product range |

| Credit Unions | 10-20% | Flexible criteria |

| Non-Bank Lenders | 10-30% | Specialist loans |

Affordability Challenges and Solutions

Affordability remains a significant challenge in real estate in new zealand. Property prices have outpaced wage growth in recent years, making traditional homeownership less accessible for many. As a result, alternative pathways are gaining traction.

Shared ownership and co-buying allow multiple parties to pool resources, making it easier to meet deposit requirements and servicing costs. Rent-to-buy schemes give buyers the opportunity to secure a property now and transition to full ownership over time. These innovative solutions are particularly helpful for young professionals, who are increasingly using creative strategies to enter the real estate in new zealand market.

- Shared ownership: Split costs, reduce barriers.

- Co-buying: Friends or family purchase together.

- Rent-to-buy: Secure home today, buy later.

Navigating Interest Rates and Loan Features

Interest rates in 2025 are expected to remain volatile, influenced by global economic trends and local market conditions. Buyers and investors must weigh the pros and cons of fixed versus floating rates. Fixed rates provide certainty, while floating rates may offer savings if the market shifts.

Modern mortgages come with features like offset accounts, redraw facilities, and flexible repayment options. These tools can help borrowers manage their cash flow and potentially reduce interest costs over the life of the loan. Regular refinancing reviews are recommended to ensure you’re always getting the best deal available in real estate in new zealand.

When negotiating your mortgage, consider loan structure, break fees, and the ability to make lump-sum repayments. Staying informed and seeking expert advice will help you navigate the ever-changing lending environment with confidence.

Types of Property and Ownership Structures

Navigating property types and ownership structures is fundamental for anyone exploring real estate in new zealand. Understanding these distinctions will help you make informed decisions, whether you’re purchasing your first home, investing, or managing property.

Residential vs. Commercial Property

In real estate in new zealand, residential and commercial properties serve distinct purposes. Residential properties include houses, apartments, and townhouses, mainly for living. Commercial properties cover offices, retail, and industrial spaces, designed for business use.

Mixed-use developments are becoming more common, blending living and working spaces. For example, Wellington has seen a rise in live-work properties, appealing to professionals seeking flexibility. Investment returns differ: residential properties usually offer stable rentals, while commercial properties may provide higher yields but come with increased regulatory requirements and market risks.

When considering real estate in new zealand, evaluate your goals, risk tolerance, and desired returns before choosing between these property types.

Understanding Freehold, Leasehold, and Unit Titles

Ownership structures in real estate in new zealand can impact your rights and responsibilities. Freehold means you own the land and buildings outright. Leasehold involves owning the buildings but leasing the land from another party, which can lead to rising ground rents and limited control.

Unit titles are common for apartments and townhouses, where you own your unit but share common areas and costs with other owners. This is managed by a body corporate, which oversees maintenance and enforces rules. For a detailed explanation, see Understanding body corporate in NZ.

| Ownership Type | Pros | Cons |

|---|---|---|

| Freehold | Full control, easier resale | Higher price, more maintenance |

| Leasehold | Lower entry cost | Lease fees, resale challenges |

| Unit Title | Shared costs, amenities | Body corporate fees, less control |

Comparing these options is crucial when buying real estate in new zealand.

Off-Plan and New Builds

Purchasing off-plan or newly built homes is a popular option in real estate in new zealand. Off-plan means buying before construction is complete, often at a lower price. This approach can offer access to modern features and government incentives for first-home buyers.

However, there are risks. Construction delays, changes to plans, or developer issues can impact your investment. It’s vital to review contracts carefully and ensure you understand the project timeline.

New builds must meet current building standards, which can reduce maintenance costs. For many, these properties represent a chance to enter real estate in new zealand with greater confidence.

Māori Land and Special Ownership Cases

Māori land holds unique importance in real estate in new zealand. Purchasing or developing Māori land involves specific legal processes, including whānau consultation and approval from the Māori Land Court.

Ownership is often collective, requiring careful management and respect for cultural values. Successful Māori land projects demonstrate how collaboration and clear communication can unlock value for communities.

Before investing, seek expert legal advice to navigate the complexities. Māori land offers distinct opportunities and responsibilities, making it a special category within real estate in new zealand.

Legal, Compliance, and Property Management Essentials

Navigating legal, compliance, and property management essentials is crucial for anyone involved in real estate in new zealand. Whether you are buying, selling, investing, or managing properties, understanding your obligations and rights protects your investment and ensures a smooth property journey.

Key Legal Requirements for Buyers and Sellers

Every transaction in real estate in new zealand begins with a legally binding sale and purchase agreement. This document outlines the terms, conditions, deposit, and settlement date. It is vital to review all clauses with a legal professional before signing.

Due diligence is essential. Buyers should obtain a LIM (Land Information Memorandum), commission a building inspection, and check the property title for encumbrances or easements. Sellers must provide accurate disclosure of any known issues or defects.

| Legal Document | Purpose | Who Prepares |

|---|---|---|

| Sale & Purchase Agreement | Sets transaction terms | Real estate agent |

| LIM | Reveals council info and compliance | Local council |

| Title Search | Confirms ownership and encumbrances | Lawyer/conveyancer |

Understanding title types is also important. Freehold, leasehold, and unit titles all have different rights and obligations. Ensuring all legal requirements are met protects your interests in real estate in new zealand.

Landlord and Tenant Obligations

Landlords and tenants in real estate in new zealand must comply with a range of legal duties. The Healthy Homes Standards set minimum requirements for heating, insulation, ventilation, moisture, and drainage in rental homes. Non-compliance can lead to penalties and disputes.

Landlords should review the Legal obligations of landlords NZ to understand responsibilities around maintenance, safety, and record-keeping. Tenancy agreements may be fixed-term or periodic, each with different notice and renewal rules.

Disputes are resolved through the Tenancy Tribunal, which handles issues from rent arrears to property damage. For more detail on compliance, see the Healthy Homes Standards explained.

Body Corporate and Multi-Unit Developments

Multi-unit real estate in new zealand, such as apartments and townhouses, is managed by a body corporate. The body corporate is responsible for maintaining common areas, setting annual levies, and enforcing rules.

Owners must attend meetings, vote on budgets, and contribute to maintenance funds. Common challenges include managing repairs, resolving disputes, and ensuring compliance with safety regulations.

Example: In Auckland, a body corporate managed a large apartment complex by creating a maintenance schedule, engaging trusted contractors, and communicating regularly with owners. This proactive approach helped avoid costly urgent repairs and increased property value. Understanding these structures is key in real estate in new zealand.

Working with Real Estate Professionals

Engaging the right professionals can make all the difference in real estate in new zealand. Licensed real estate agents guide buyers and sellers through negotiations, paperwork, and compliance checks. Property managers oversee rental properties, ensuring legal standards are met and rent is collected on time.

Fees and commissions are typically outlined in a service agreement. It is wise to compare services, check references, and understand the scope of each contract before signing.

Professional support streamlines complex transactions and provides peace of mind for all parties involved in real estate in new zealand.

Future Outlook: Trends Shaping Real Estate Beyond 2025

The future of real estate in new zealand is set for transformation, driven by technology, sustainability, shifting demographics, and evolving policy. As we look beyond 2025, industry professionals, investors, and homeowners must prepare for rapid changes. Understanding these trends is essential for making informed decisions in the coming years.

Technology and Digital Transformation

The adoption of proptech is reshaping real estate in new zealand. Virtual tours, AI-powered valuations, and blockchain for secure transactions are becoming standard tools for buyers and sellers. These innovations make property transactions more transparent and efficient.

Digital platforms are enabling clients to search, buy, and manage properties online. For example, the use of online auction platforms has surged, allowing buyers from across the country to participate with ease. This digital shift is expected to accelerate, influencing every stage of the property journey.

Sustainability and Green Building

Sustainability is a growing priority in real estate in new zealand. Buyers are increasingly seeking energy-efficient homes, and developers are responding with green building practices. Features like solar panels, smart water systems, and eco-friendly materials are now mainstream.

Government incentives support the construction of sustainable homes, encouraging net-zero developments, particularly in cities like Christchurch. The demand for green properties is likely to intensify, making sustainability a key driver of value for both investors and homeowners.

Demographic and Lifestyle Shifts

Demographic changes are influencing real estate in new zealand in significant ways. Population growth, urbanisation, and changing household structures are reshaping demand patterns. Millennials and Gen Z buyers are prioritising flexibility, connectivity, and affordability.

There is a noticeable rise in co-living models and alternative housing arrangements, especially in urban centres. These trends are expected to continue as younger generations enter the property market and as remote work remains popular, shifting preferences towards lifestyle-oriented locations.

Policy and Economic Influences

Government policy and economic cycles will remain central to the future of real estate in new zealand. Upcoming regulations, such as changes to tax and ownership laws, can impact investment returns and market stability.

Economic resilience is crucial, and the market has learned valuable lessons from previous property cycles. For commercial property, projected growth rates and market values can be explored in the Statista Commercial Real Estate Forecast, which provides insight into future market drivers and risks.

Opportunities and Challenges Ahead

Looking forward, real estate in new zealand will offer both new opportunities and emerging challenges. Regional markets and innovative property types, such as mixed-use developments, may present robust growth options.

Buyers and investors must remain alert to risks like market volatility and regulatory changes. Expert predictions suggest that adaptability and a focus on long-term value will be vital for success as the landscape evolves beyond 2025.

As you navigate the opportunities and challenges of New Zealand’s real estate market in 2025, having reliable answers and up-to-date insights can make all the difference—whether you’re buying your first home, investing, or managing property. Throughout this guide, we’ve unpacked key trends, regulatory updates, and practical steps for every stage of your property journey. If you want to stay informed about the latest body corporate developments, connect with trusted contractors, or dive deeper into expert advice tailored to your needs, you’ll find everything you need at Buying Property in New Zealand.